Half-life is how long a pair stays interesting

A practical tour of mean-reversion timescales and what they imply for your holding period.

If you trade pairs and you do not know the half-life of your spread, you do not know when to exit.

Half-life is the single most useful number in pairs trading that almost nobody talks about. It tells you the expected time for a shocked spread to revert halfway back to its equilibrium. If the half-life of your BTC/ETH spread is twelve hours and you are holding a position open for four days, the trade is no longer about the mean-reversion you entered on. It is about something else. Usually leverage.

This post explains what half-life is, how to compute it from your own data and how to use it to set holding-period rules.

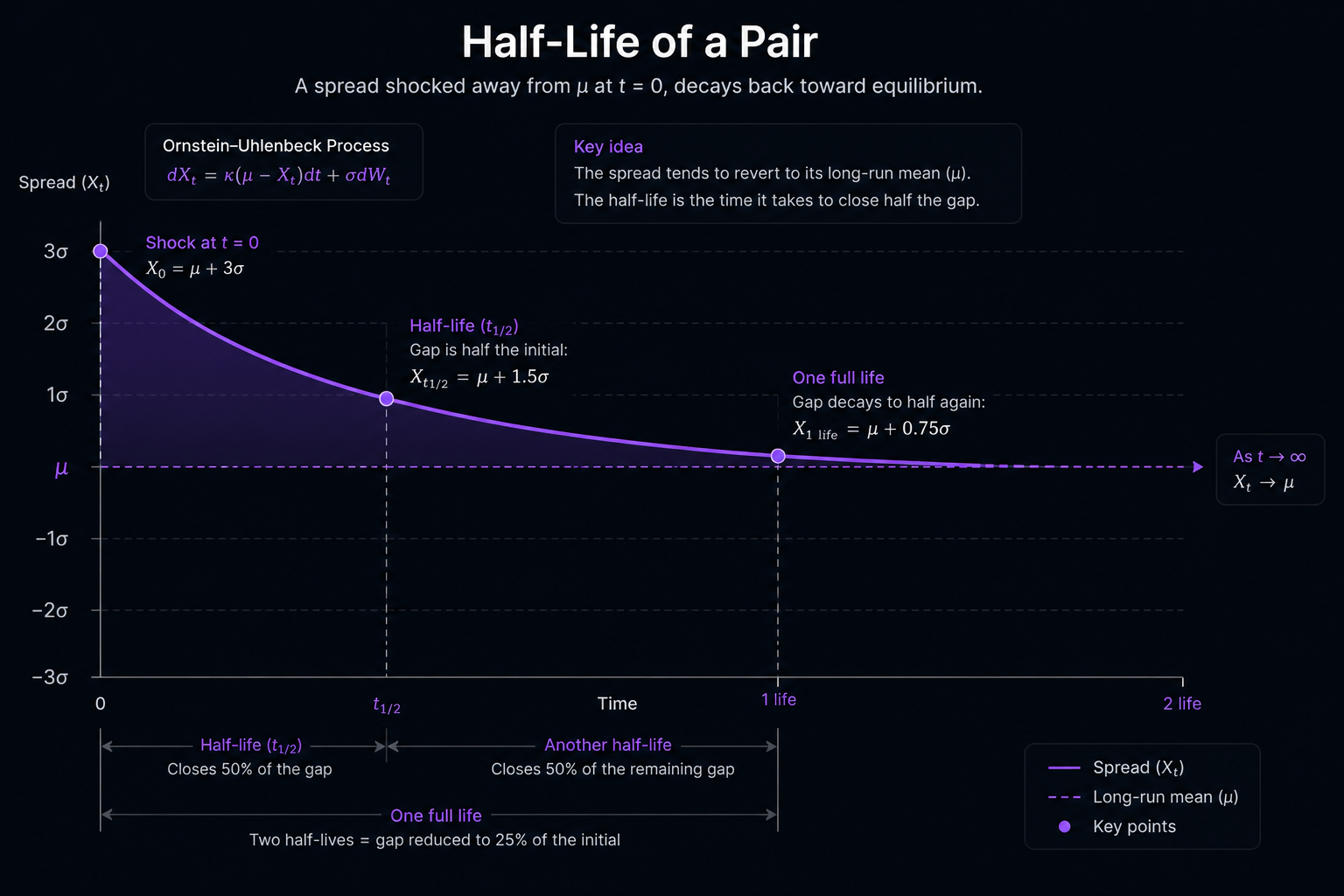

The Ornstein-Uhlenbeck process in one minute

A mean-reverting spread is modelled as an Ornstein-Uhlenbeck process (Uhlenbeck and Ornstein 1930):

dZ(t) = θ × (μ − Z(t)) × dt + σ × dW(t)

What this says in English. The spread Z moves around. It has a long-run mean μ. The further the spread is from the mean, the harder it is pulled back; the strength of that pull is θ. There is also random noise of size σ that pushes the spread around and gives it texture.

The single number that determines how fast the spread reverts is θ. Large θ means strong pull, fast reversion. Small θ means weak pull, slow reversion. From θ you compute the half-life:

τ ≈ ln(2) / θ

The half-life is the expected time for a shocked spread to decay halfway back to where it usually sits. After one half-life the shock is half gone. After two half-lives, three-quarters gone. After three half-lives, seven-eighths. The decay is geometric.

How to compute it from your own data

You probably do not have continuous-time data. You have bars. Fit a discrete-time AR(1) on the empirical spread:

ΔZ(t) = κ + φ × Z(t−1) + η(t)

The half-life in the discrete form is:

τ = −ln(2) / ln(1 + φ)

That is it. One AR(1) fit on your spread series gives you a number in the same units as your bars. If you used 5-minute bars and got a half-life of 24, the spread reverts halfway in two hours. If you used hourly bars and got 18, the half-life is 18 hours.

For the spread to be statistically mean-reverting at all, you need a negative φ in the AR(1) fit (because ln(1 + φ) must be negative for τ to be positive and finite). If φ is close to zero, the spread is close to a random walk and the half-life is enormous. That means the pair is not actually tradeable; you would be holding through arbitrary excursions.

Matching holding period to half-life

The standard advice from the literature: holding periods should be on the order of one to several half-lives. The exact multiplier is a tuning parameter, usually called k. Common practice uses k between 2 and 4.

If the half-life of your spread is 12 hours and k = 3, you close any position that has been open for 36 hours regardless of where the z-score sits. This is a half-life timeout. It keeps capital from being trapped in trades where the assumed mean-reversion has not materialised. The cost is that occasionally you exit a position that would have eventually reverted. The benefit is that you do not bleed capital on positions that have stopped being trades and become bets.

Half-life timeouts pair naturally with z-score thresholds and with closed-form optimal-stopping rules. Bertram (2010) derives the optimal entry and exit thresholds under the OU model analytically. The optimal thresholds end up depending on θ (and therefore on the half-life) and on the transaction cost. The heuristic of ±2σ for entry has no theoretical basis. The Bertram-optimal entry threshold depends on how fast your spread reverts and how much it costs you to trade in and out.

Why this matters for crypto perps

Equity pair half-lives are typically days to weeks. Crypto pair half-lives are shorter. Hours to days for major pairs; tens of minutes to hours for actively-trading altcoin pairs. This is a substrate property, not a strategy choice. It means that the holding-period rules you read about in the equity literature do not transfer directly. A two-week holding limit from an equity pairs paper is forever in crypto perp time.

It also means that the half-life is itself non-stationary. The half-life of BTC/ETH in a calm regime is not the half-life in a chaotic regime. The number you fitted last week is not the number that applies this week. A platform that uses a fixed half-life for its holding rules is using a stale number. A platform that re-fits the half-life as the regime evolves uses a current one.

The takeaway

If you read one number off your pair s spread, read the half-life. It tells you how long the trade has before it stops being a trade. The rest of your rules (entry threshold, exit threshold, position size) should be functions of it, not independent of it.

The full formal treatment is in the technical guide. The implementation paper covers how half-life pairs with optimal stopping and with risk-management overlays.

References

- Uhlenbeck, G.E. and Ornstein, L.S. (1930). On the theory of the Brownian motion. Physical Review 36(5).

- Bertram, W.K. (2010). Analytic solutions for optimal statistical arbitrage trading. Physica A 389(11).

- Engle, R.F. and Granger, C.W.J. (1987). Co-Integration and Error Correction. Representation, Estimation and Testing. Econometrica 55(2).

- Vidyamurthy, G. (2004). Pairs Trading. Quantitative Methods and Analysis. Wiley.

- Bonton AI, Hedgicore Research (2026). Statistical Arbitrage. A Technical Guide. v1.0.

Hedgicore is a real-time pairs analytics platform powered by the Hedgicore Engine. Built by the team at Bonton AI.

Risk disclaimer: Hedgicore is an analytics platform. It does not execute trades or provide financial advice. All trading carries risk of loss.